If you're a homeowner getting ready to move, one question usually comes first: should you buy your next home before you sell, or sell your current house before you start looking?

There's no single right answer. The best call depends on your finances, your local market, and your timeline. And a trusted agent can help you weigh all of it.

But in a lot of cases these days, selling first puts you in the stronger spot.

The Advantages of Selling First

Selling is usually the trickier half of a move today, so getting it done first clears your biggest hurdle. And that’s especially true right now, because there are more homes for sale than there are buyers, which means houses are taking longer to sell than they did a year or two ago.

So how does leading with your sale pay off? Let’s start with the money.

1. You Won’t Get Stuck Paying Two Mortgages

Buy before you sell, and you could end up carrying two mortgages at once. And especially since houses are staying on the market longer these days, that overlap may drag on for more time than you’d planned. And if unexpected repairs come up, it could get even more expensive.

Selling first takes that risk off the table, so you’re not multitasking homeownership. As Ramsey Solutions puts it:

"It's best to sell your old home before buying a new one to avoid unnecessary risks and possible headaches."

2. You Can Use Your Equity To Fuel Your Move

This is always true, but one of the biggest perks of selling first is that you’ll know exactly how much money you're walking away with. And one of the big figures that matters in that conversation is how much equity you have in your current place.

Equity is basically your house’s value minus what you still owe on your mortgage. And it adds up fast. According to Realtor.com, homeowners who’ve been in their home for 5 years have about $180,000 in equity on average. And those who’ve had their home for 6-10 years? They have over $340,000.

After you sell, you can use that money to cover your down payment or even buy your next home in cash. And knowing that profit up front helps you plan your next move.

3. Your Offer Will Be Hard To Pass Up

When your house is already sold, you don’t have to make your offer contingent on that sale. In a market where buyers are taking their time, that’s exactly what a seller wants to see.

Picture it from the seller’s side. If their house has been sitting for a while, they’ll gravitate toward the offer most likely to close without a snag.

That can also give you room to ask for a little more, like repairs, since a motivated seller would rather keep things moving than lose you and wait for another offer to come in. Your agent can help you make the most of your upper hand in that scenario.

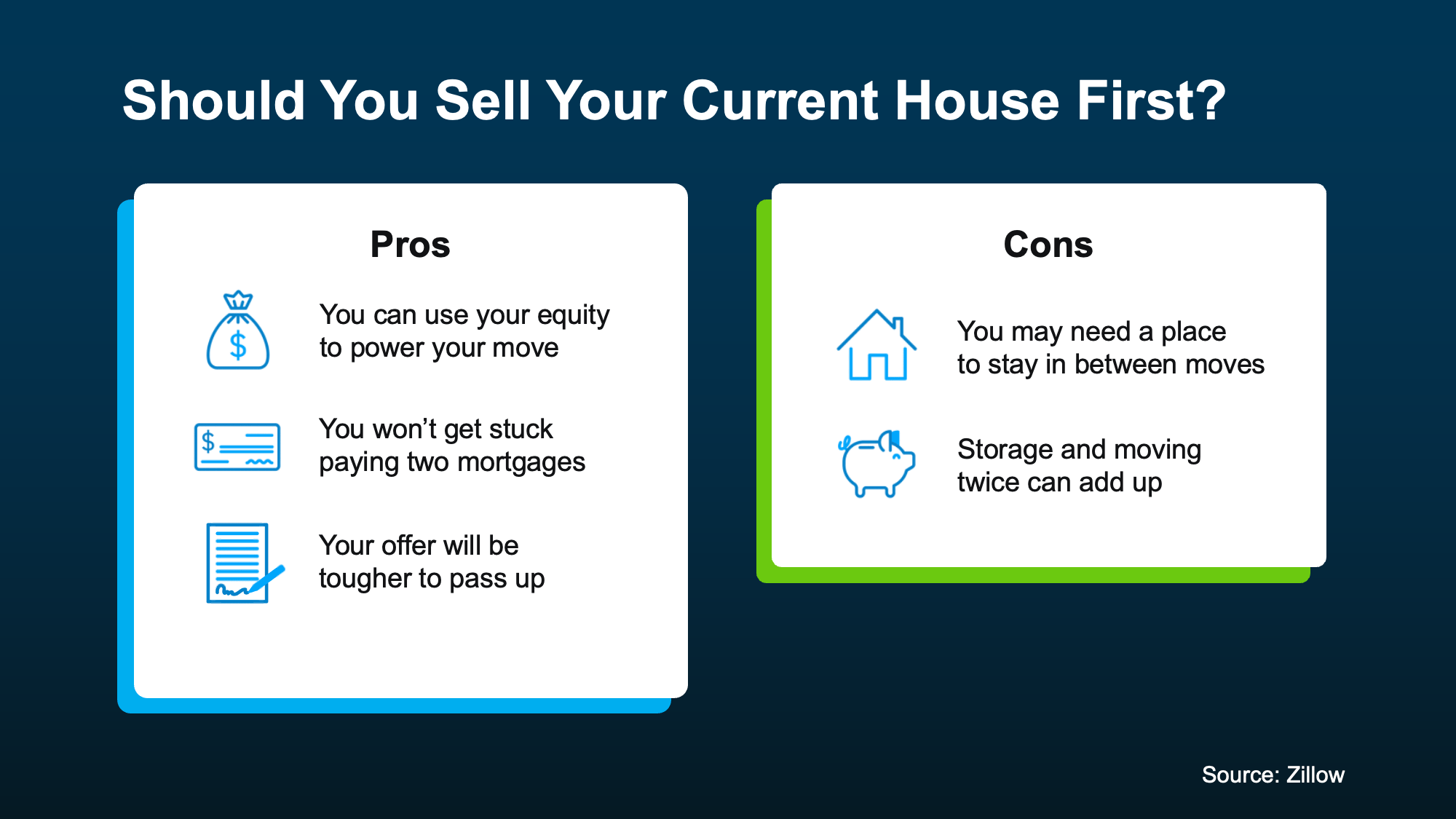

Is There a Catch?

Selling first has its tradeoffs too, and it helps to see the pros and cons side by side before you decide. Here’s a quick breakdown based on information from Zillow (see visual below):

The cons are manageable with the right plan, so talk about them with your agent. They can help you negotiate things like a rent-back, where you stay in your house for a set time after closing, or line up flexible closing dates to keep the transition smooth.

Bottom Line

There's no one-size-fits-all answer to buying and selling at once. But for a lot of homeowners, leading with the sale makes moving easier on their mind and their wallet.

Let’s connect, so you can navigate selling and buying with more confidence, more financial power, and less stress.