If you’re planning to buy your next home soon, you’ve probably heard the old rule about saving 20% for your down payment.

The truth is, you usually don’t have to. Plenty of loan options let qualified buyers put down much less. But a lot of repeat buyers are choosing to put down 20% anyway.

So, why are they if they don’t have to?

Two reasons. They know a bigger down payment pays off, and after years in their current house, they’ve built up enough equity that it’s finally possible.

Repeat Buyers Put More Money Down

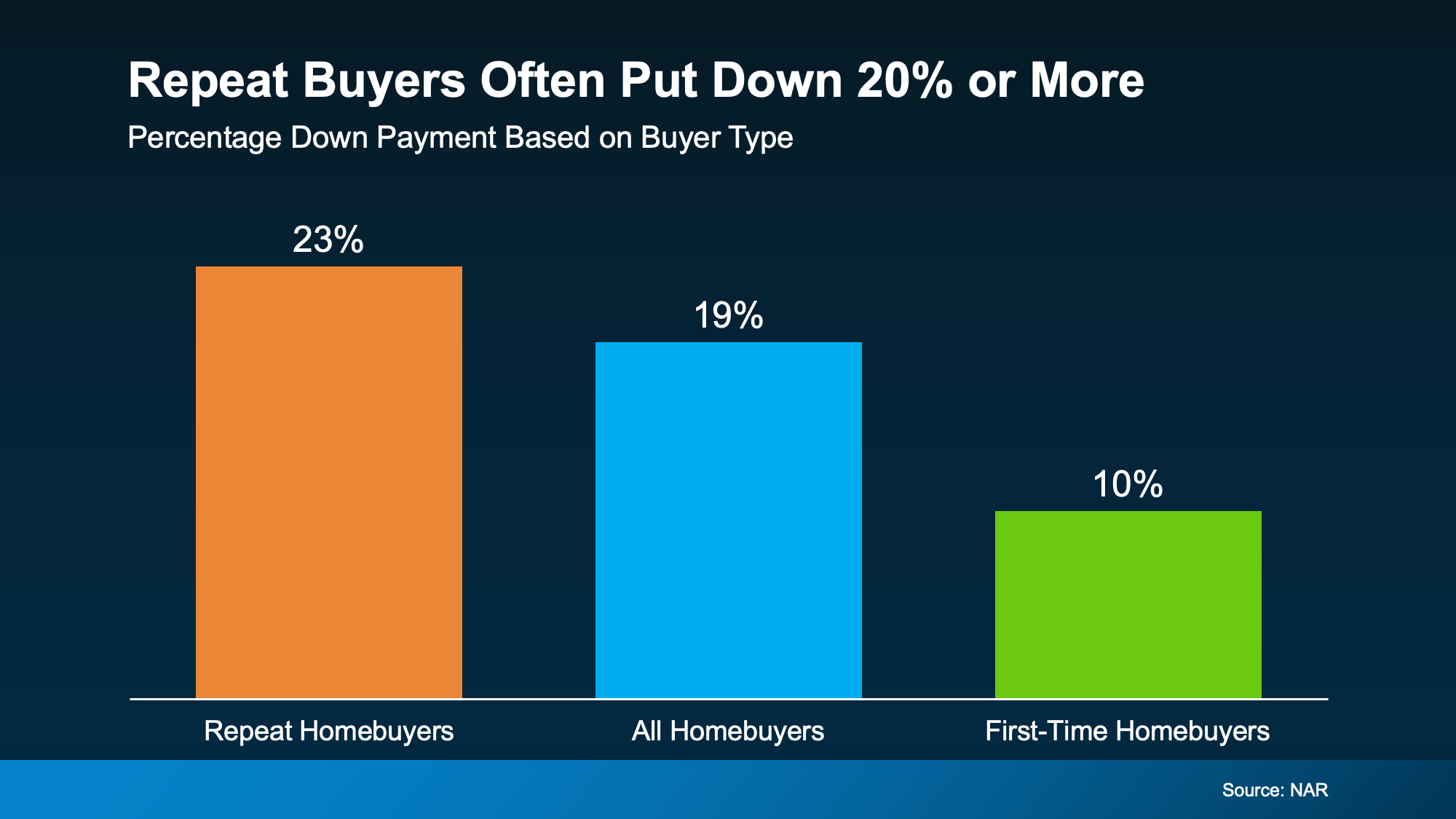

According to the National Association of Realtors (NAR), the typical repeat buyer puts down 23%when they buy a home (see graph below):

That’s more than double the 10% they may have put down as a first-time buyer. So, how do they manage it? Their equity.

When you’ve owned a house for a while, two things tend to happen. One, you pay down your mortgage, and two, your home’s value climbs. The difference between what you still owe on your mortgage and what your house is worth is your equity. And the longer you’ve lived in your house, the bigger that number grows.

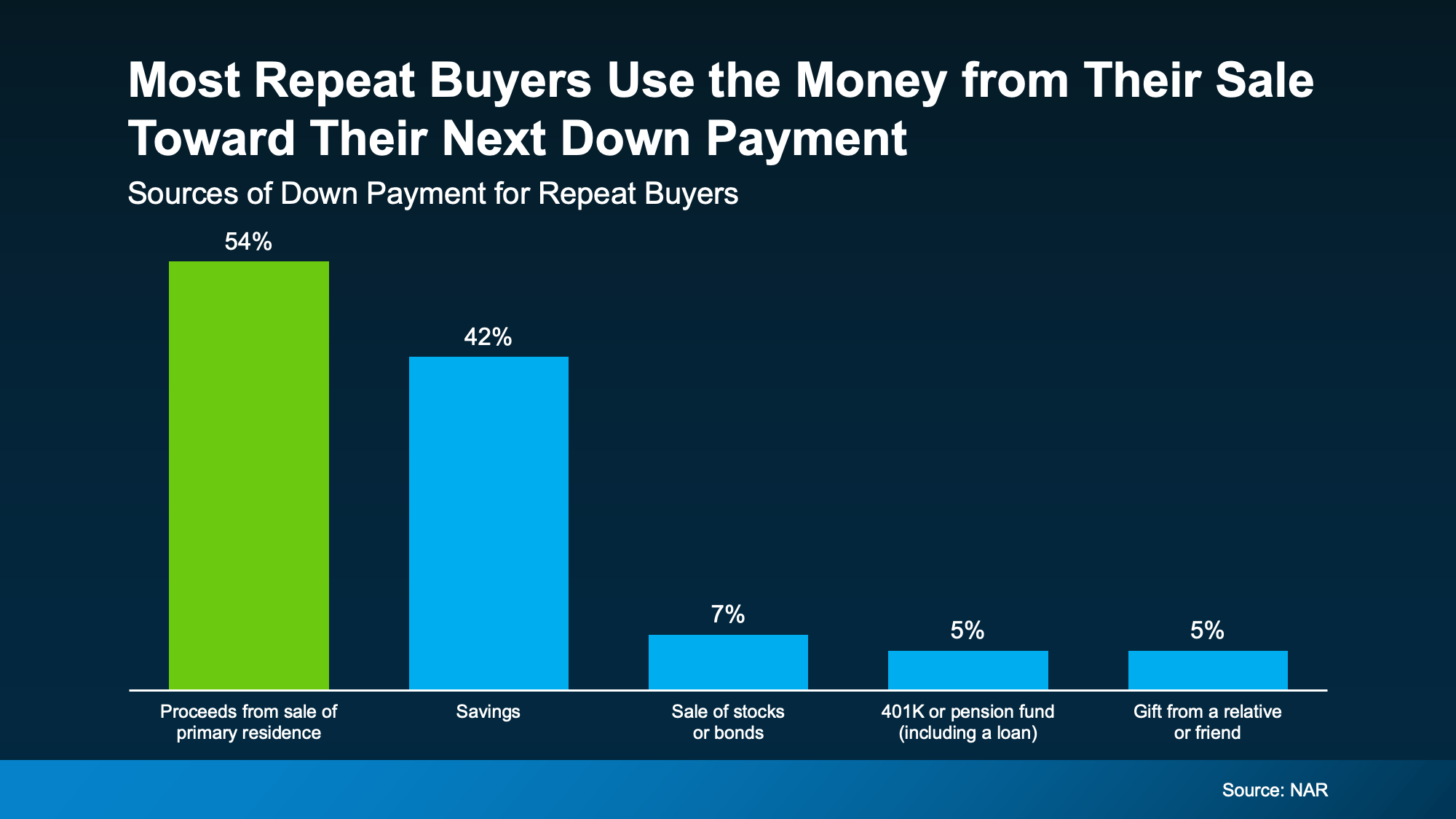

When you sell, your equity turns into cash. And NAR data shows most repeat buyers put it straight toward their next down payment (see chart below):

First-time buyers don't have that springboard yet, and that's normal. But if you already own, you may be holding more buying power than you think because of it.

And if putting 20% down is finally possible, it may be worth at least considering. Here’s why. Let’s go over what you get in return.

4 Perks of Putting 20% (or More) Down

As Redfin explains, putting more down pays off in a few ways:

A smaller monthly payment. The more you put down, the less you borrow at today’s rates. And if taking on a higher mortgage rate is one of the reasons you’re debating whether to move, that’s a win.

Paying less interest. A smaller loan can also carry less interest across the life of your mortgage. If you put 20% down, you’ll only pay interest on the remaining 80%. Put 5% down and you’ll pay interest on the remaining 95%, which will cost you more over the lifetime of the loan.

No private mortgage insurance (PMI). When you put down less than 20% on a conventional loan, lenders usually add a monthly fee called private mortgage insurance. With 20% down, PMI isn’t required and that saves your money every month.

A stronger offer. A larger down payment can make your offer more attractive, since sellers tend to read it as a sign your financing is solid and the deal is more likely to close.

Bottom Line

So, no. You don't need to put 20% down to buy your next home. But you may want to. If your equity puts it within reach, going bigger can lower your costs and make moving more doable than you think – even with today’s rates.

A trusted lender can run the numbers on your financing. And when you want to know what your current house could add to your next down payment, let's talk.